Futures: Overnight, LME copper opened at $9,942/mt, rose to a high of $9,971/mt during the session, and fell to a low of $9,900/mt at the close, ending at $9,907/mt. The overall trend initially fluctuated upward before pulling back. The decline was 1.86%, with a trading volume of 31,000 lots and open interest of 303,000 lots. Overnight, the most-traded SHFE copper 2505 contract opened at 81,670 yuan/mt, rose to a high of 81,870 yuan/mt during the session, and fell to a low of 81,350 yuan/mt at the close, ending at 81,520 yuan/mt. The overall trend fluctuated downward. The decline was 1.08%, with a trading volume of 62,000 lots and open interest of 240,000 lots.

[SMM Copper Morning Meeting Summary] News: (1) After the US stock market closed on Wednesday, March 26, Eastern Time, according to CCTV News, US President Trump signed an executive order at the White House, announcing a 25% tariff on all imported cars. The related measures will take effect on April 2. According to CCTV, Trump stated that the car tariffs will be permanent. He said that if cars are made in the US, no tariffs will be levied. This means that the new tariffs will apply to all non-US-made cars.

(2) The US has added more than a dozen Chinese entities to the export restriction list of the US Department of Commerce. In response, a spokesperson for the Chinese Ministry of Foreign Affairs stated that China firmly opposes this and strongly condemns it. We urge the US to stop generalizing the concept of national security, stop politicizing, instrumentalizing, and weaponizing economic, trade, and technological issues, and stop abusing various sanction lists to unreasonably suppress Chinese companies. China will take necessary measures to resolutely safeguard the legitimate rights and interests of Chinese companies.

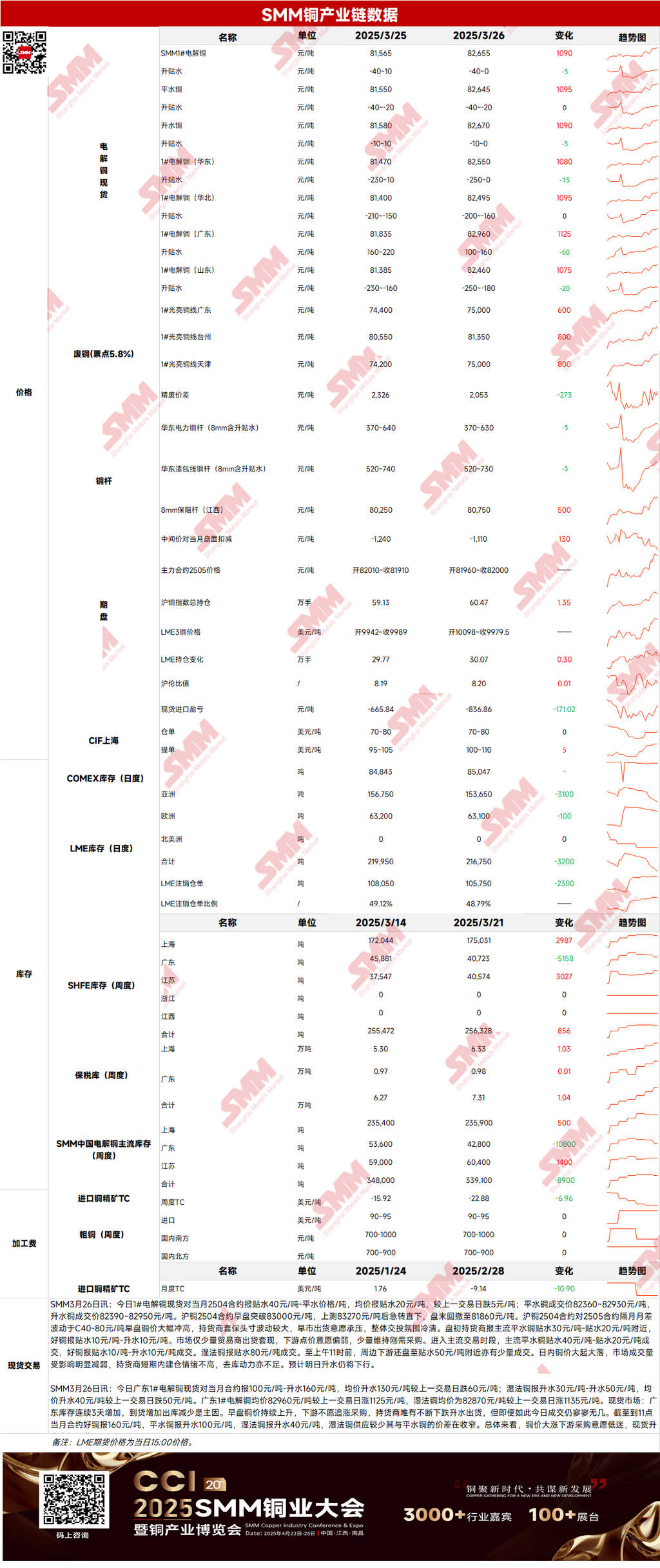

Spot: (1) Shanghai: On March 26, spot prices of #1 copper cathode against the front-month 2504 contract were reported at a discount of 40 yuan/mt to parity, with an average discount of 20 yuan/mt, down 5 yuan/mt MoM. Yesterday, copper prices fluctuated sharply, significantly weakening market trading volume. Suppliers showed low sentiment for short-term inventory building, and destocking momentum was also insufficient. Spot premiums are expected to continue declining today.

(2) Guangdong: On March 26, spot prices of #1 copper cathode in Guangdong against the front-month contract were reported at a premium of 100 yuan/mt to 160 yuan/mt, with an average premium of 130 yuan/mt, down 60 yuan/mt MoM. Overall, downstream purchase willingness was low amid the sharp rise in copper prices, and spot premiums fell significantly.

(3) Imported copper: On March 26, warrant prices were $70-80/mt, QP April, with the average price flat MoM; B/L prices were $100-110/mt, QP April, with the average price up $5/mt MoM; EQ copper (CIF B/L) was $40-50/mt, QP April, with the average price flat MoM. Offers referred to cargoes arriving in mid-to-late March and early April. According to market news, long-term contract supply from South America decreased again yesterday, with almost no offers for far-month registered pyrometallurgy B/Ls, only scattered EQ and warrant offers, but transactions were also hard to hear. Buyers mostly remained in a wait-and-see state due to large fluctuations in copper prices and no significant inventory building demand.

(4) Secondary copper: On March 26, secondary copper raw material prices rose 600 yuan/mt MoM. Bare bright copper prices in Guangdong were 74,900-75,100 yuan/mt, up 600 yuan/mt from the previous trading day. The price difference between primary metal and scrap was 2,053 yuan/mt, down 273 yuan/mt MoM. The price difference between primary and secondary copper rods was 1,610 yuan/mt. According to the SMM survey, as copper prices fell back from highs, secondary copper rod enterprises continued to sell off goods as they did yesterday, but downstream demand led to mediocre intraday transactions.

(5) Inventory: On March 26, LME copper cathode inventories decreased by 3,200 mt to 216,750 mt; on March 26, SHFE warrant inventories decreased by 3,572 mt to 139,568 mt.

Price: On the macro front, Trump announced a 25% tariff on imported cars on Wednesday, and insiders said the US will accelerate the imposition of copper tariffs, several months earlier than expected, raising concerns about escalating trade tensions and slowing global economic growth. The uncertainty brought by copper tariffs pushed Comex copper prices to a new historical high, and the price spread between Comex and LME copper continued to widen. On the supply side, copper prices surged sharply in the early session, with large fluctuations in suppliers' hedging positions, putting pressure on their willingness to sell, and the supply side remained relatively deadlocked. On the demand side, downstream willingness to fix prices was weak, with only a small amount of just-in-time procurement maintained. Intraday copper prices fluctuated sharply, significantly weakening market trading volume, and overall demand performance was mediocre. In terms of prices, copper prices are expected to continue their downward trend today, but the overall downside space is limited.

》Click to view the SMM Metal Database

[The above information is based on market collection and comprehensive evaluation by the SMM research team. The information provided in this article is for reference only. This article does not constitute direct advice for investment research decisions. Clients should make decisions cautiously and not use this as a substitute for independent judgment. Any decisions made by clients are unrelated to SMM.]